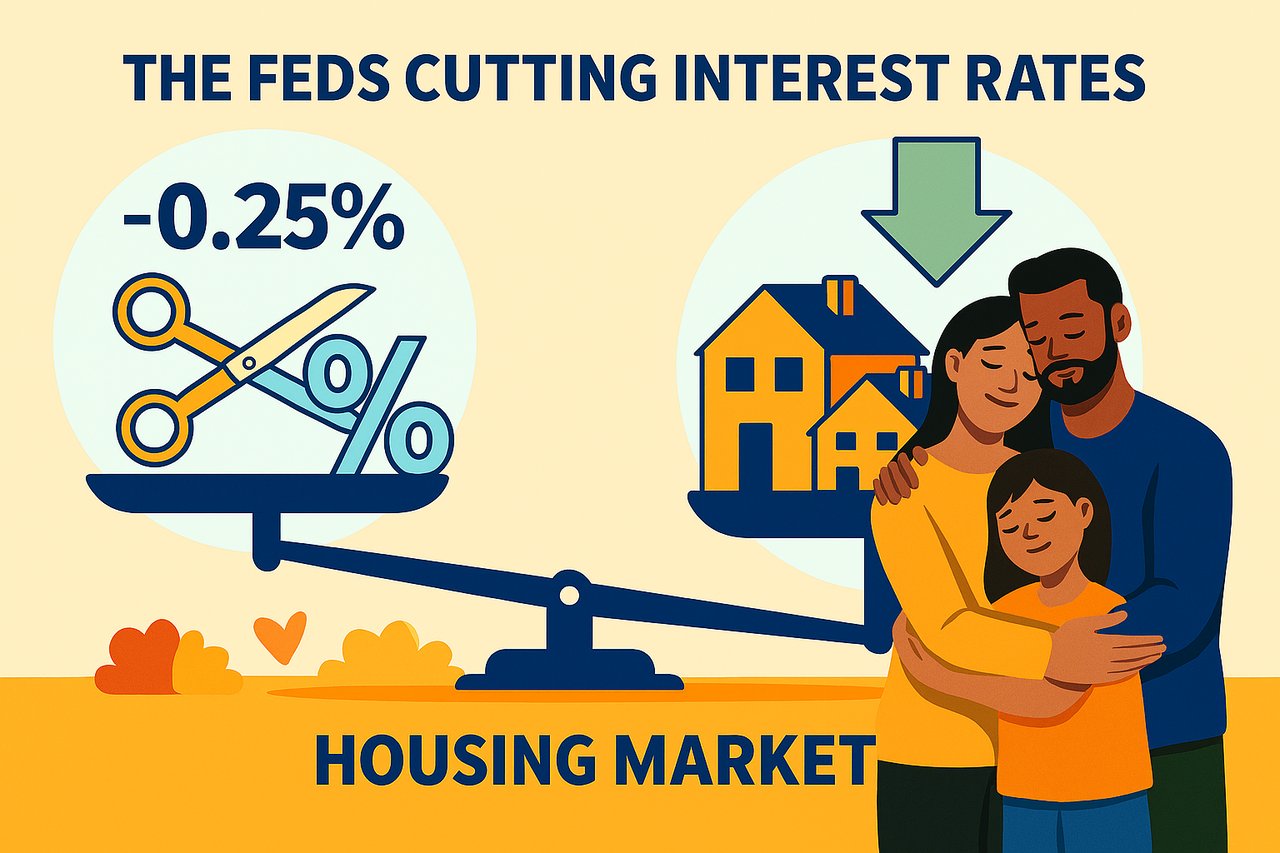

The Federal Reserve (and central banks worldwide) just announced a quarter-point (0.25%) reduction in interest rates. While the move may appear modest, the effects on the housing market can be significant. Housing is one of the sectors most sensitive to changes in borrowing costs, and even small rate shifts can influence affordability, buyer demand, and overall market sentiment.

Lower Borrowing Costs Spark Buyer Interest

With mortgage rates closely tied to interest rate movements, this reduction will make financing a home purchase slightly more affordable. For example, on a $500,000 mortgage, the cut could reduce monthly payments by $75–$100 depending on the terms. Over time, that adds up to thousands in savings—an incentive strong enough to bring many hesitant buyers back into the market.

First-time buyers, in particular, stand to benefit. A lower monthly payment may be the deciding factor in their ability to qualify for a loan. Meanwhile, move-up buyers may see this as an opportunity to stretch their budgets and consider larger homes or more desirable neighborhoods.

Refinancing Activity on the Rise

The rate cut doesn’t just impact new buyers—it also encourages existing homeowners to refinance. Even a 0.25% reduction can be worth locking in for those who want to lower their monthly payments, shorten their loan terms, or move from an adjustable-rate mortgage to a fixed one. Increased refinancing activity frees up cash flow for households, potentially boosting consumer spending in other areas of the economy.

Increased Competition in Tight Markets

In many regions, housing inventory remains constrained. Lower borrowing costs could drive more buyers into the market, increasing competition for limited listings. This heightened demand may lead to bidding wars, faster sales, and upward pressure on prices. Sellers benefit from this environment, but buyers may find themselves paying more despite the rate relief.

Affordability Sees a Temporary Lift

Housing affordability has been a growing concern, with home prices rising faster than incomes. A 0.25% rate cut helps by trimming monthly costs for buyers, but it doesn’t fully solve the issue. In fact, if demand surges without a corresponding increase in supply, the affordability gains may be short-lived as prices rise further.

Confidence and Market Sentiment Improve

Beyond the math, interest rate cuts send a strong psychological signal. Buyers and sellers often interpret them as a sign that financing conditions will remain favorable. This renewed confidence can lead to more transactions, greater activity in open houses, and increased momentum across the market.

The Federal Reserve’s (and other central banks’) decision to reduce rates by a quarter-point is already shaping the housing market. Buyers enjoy slightly lower costs, homeowners consider refinancing, and sellers see stronger demand for their listings. Still, the long-term impact depends on whether housing supply can keep pace with renewed demand.

Even small rate changes remind us how closely tied real estate is to monetary policy. For anyone considering buying, selling, or refinancing, now is the time to watch the market carefully and act strategically.